Beyond Adaptation: How BESS trading strategies are evolving under Schedule & Dispatch

The Schedule & Dispatch (S&D) programme introduced on 13 November 2025 represented a significant step forward for battery energy storage assets in the SEM. By improving the ability of battery storage (BESS) assets to participate directly in the energy markets, S&D has created new opportunities for asset owners and optimisers to capture value through wholesale trading while providing additional flexibility to the system.

However, S&D has not been the only market change, shaping the opportunity for batteries. The continued growth of renewable generation, particularly solar, has fundamentally changed the shape of the electricity market. Increased solar output has created a more pronounced midday price depression, while demand continues to drive evening peaks. This changing generation profile is creating new opportunities for batteries to capture value across multiple periods of the day.

In our previous analysis (read here: Adapting to Opportunity: A first look at the impact of Schedule & Dispatch on BESS assets in the SEM), we examined the first 50 days following the implementation of S&D. At that stage, asset owners and optimisers were adapting to the new market structure, while the TSO continued to embed new operational processes. We saw an increase in traded volumes and trading revenues, with assets beginning to engage more actively in the energy markets. This trend has continued with April being the month with the highest trading volume, with a 43% increase on what we seen in December (the first full month of S&D).

The analysis in this Insight is based on publicly available data. ElectroRoute does not have access to individual asset trading strategies or operational data, and assumptions have been made where required. Revenue calculations assume firm access and use a simplified view of SEM charges, which provides a slight overestimation of Traded revenue.

Market Insight

Since the implementation of S&D, traded BESS volumes have continued to increase across the energy markets. As can be seen in Figure 1, the Day Ahead (DA) market remains the dominant source of traded volume and continues to grow steadily, while Intraday Auction 1 (IDA1) remains a smaller but important optimisation opportunity. Since this introduction of S&D, we have seen over twice as much traded volume by BESS units in the DA market compared to the three IDA markets combined.

The ability to adjust positions closer to real time allows optimisers to respond to changing market conditions, lock in value, and optimise traded positions without necessarily requiring additional cycling of the asset.

The continued growth in day-ahead and intraday participation demonstrates that BESS assets are becoming increasingly integrated into the wider energy market, rather than operating solely around system service revenues. We still see the level of churn across the markets to be a fraction compared to other markets like Great Britain and Germany. This is driven by two key factors: a lack of liquidity and sophisticated trading products to allow for linked bids. Which remains a limiting factor for the BESS market in Ireland.

Trading Revenues remain linked to Market Dynamics

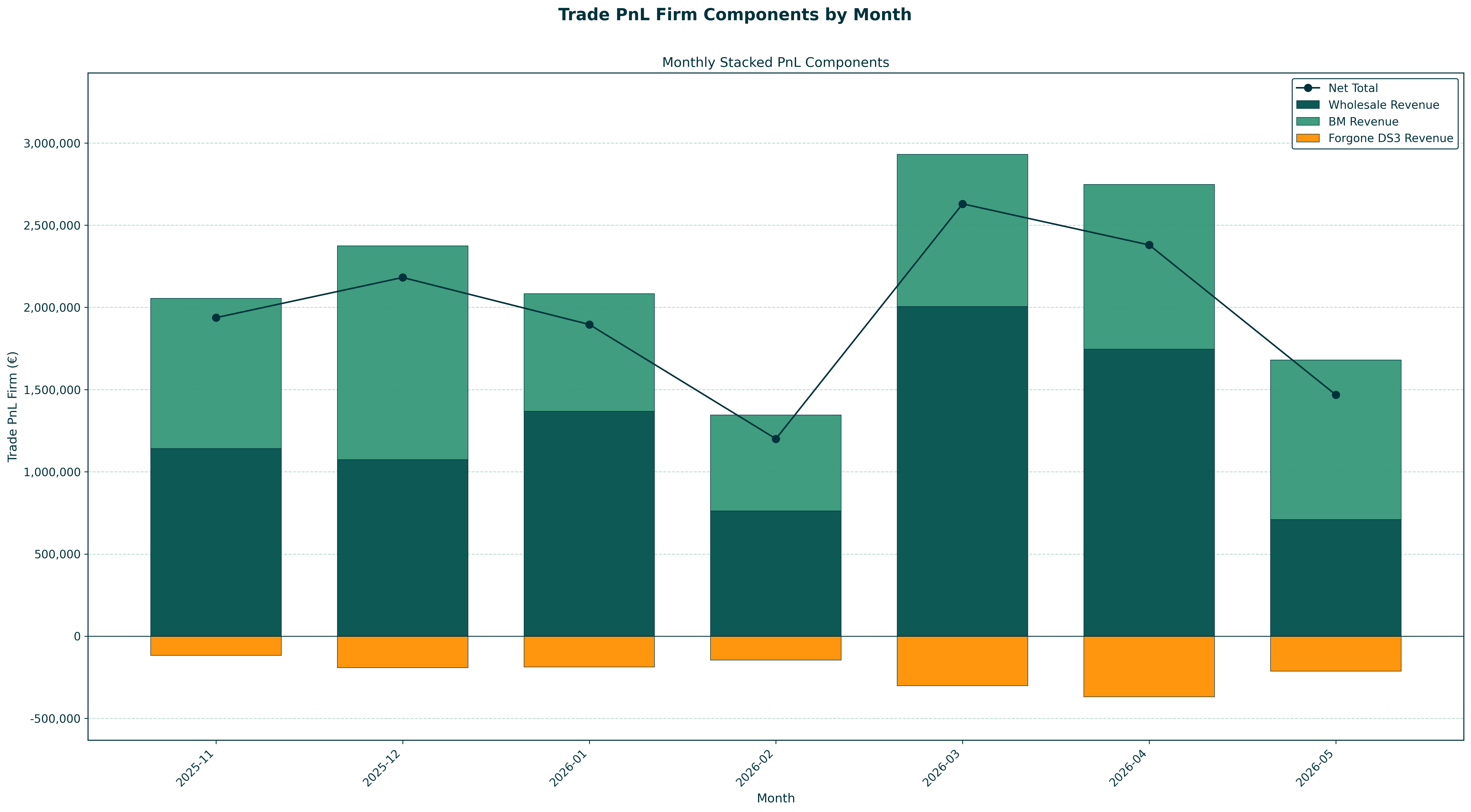

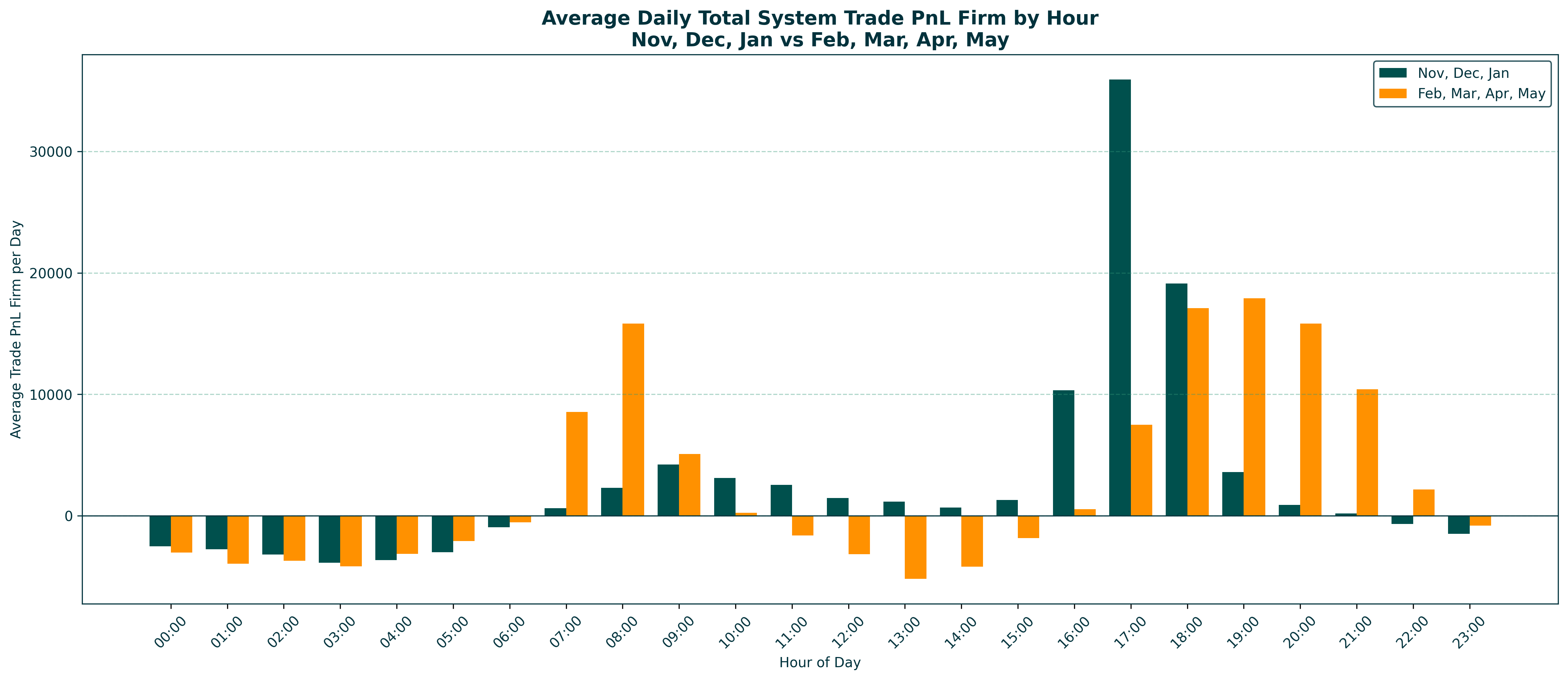

Monthly trading revenues across the BESS fleet remain variable, driven by the level of arbitrage opportunity available in the market. We have seen an increase in strong revenue opportunities, but also an increase in risk. Since the introduction of S&D until the end of May 2026, there have been 30 days with a total system wide negative Trade PnL. One day resulted in the BESS fleet running a total loss of over €65k.

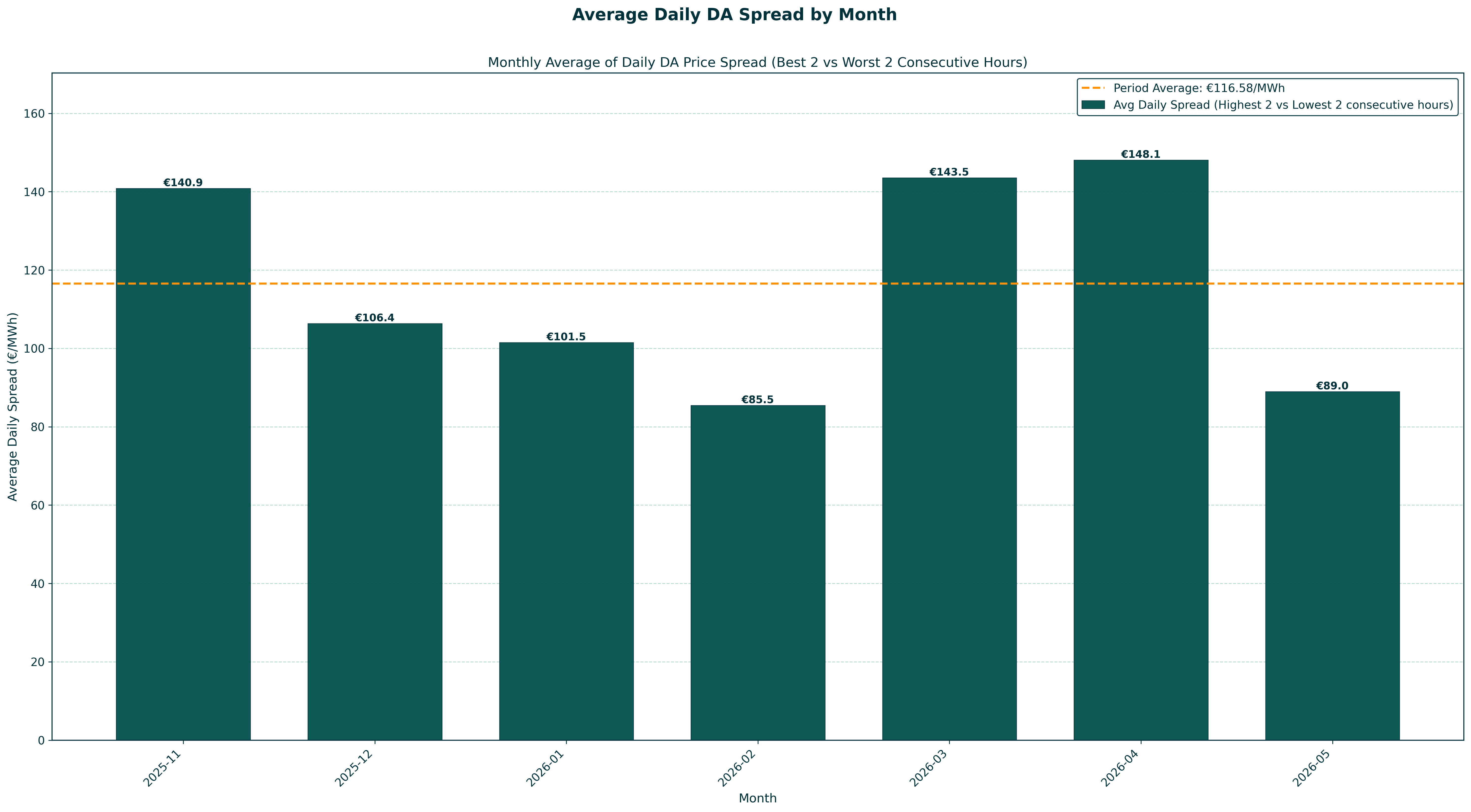

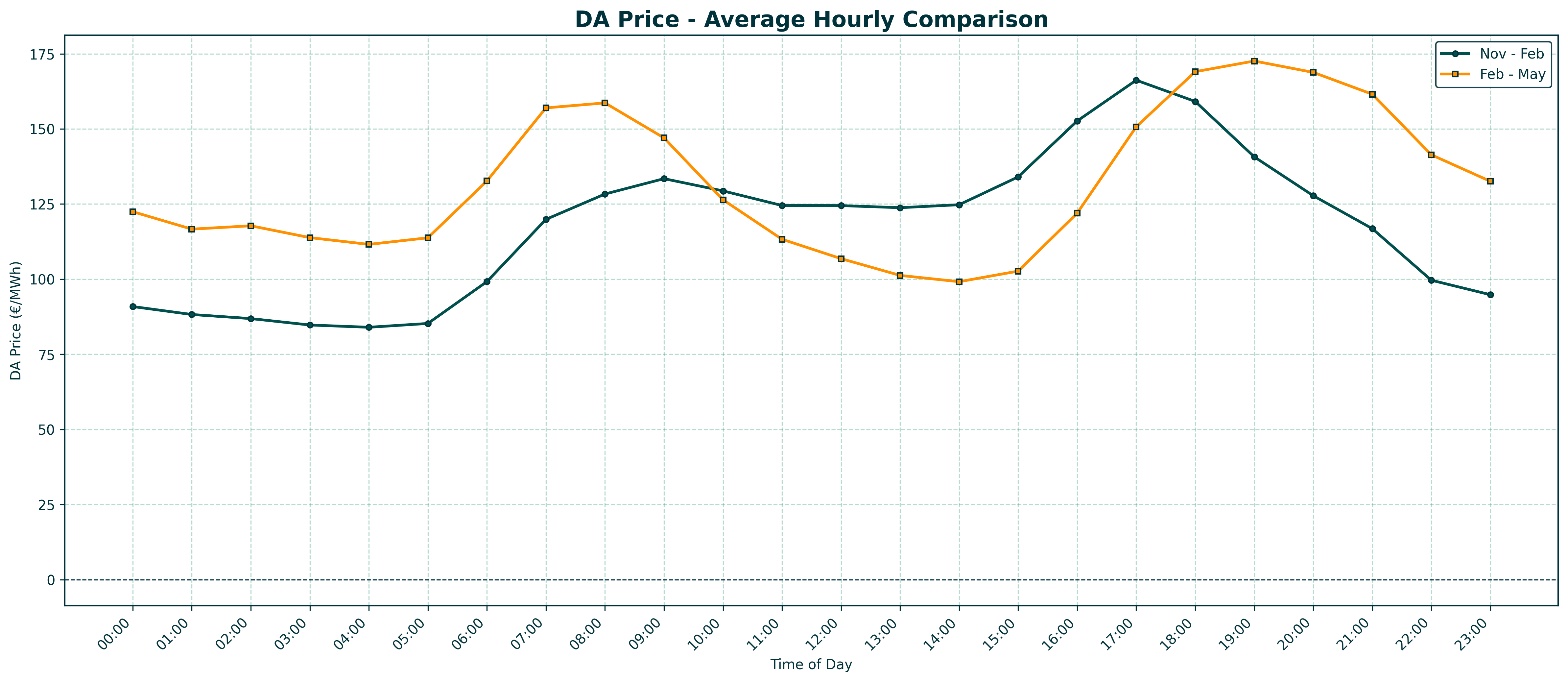

March and April 2026 proved to be particularly strong months for BESS trading, supported by high renewable generation levels and strong morning and evening demand. An increase in price spreads resulted in March having over twice the total Trade PnL of February. It’s not surprising that February was the worst month we have seen for daily DA market price spreads since the introduction of S&D, and also the worst total Trade PnL.

Access to Balancing Mechanism (BM) revenue is another key driver of monthly earnings. While participation in the BM is not driven by market economics and is instead largely determined by the TSOs operational processes and system constraints, it can still provide significant value to assets. From the start of S&D to the end of May, wholesale revenue was around 40% larger than BM revenue, though BM revenue made up a more significant portion of revenue in May with a reduction in wholesale profits.

Non-firm assets are exposed to the spread between the imbalance price and the wholesale market price when they are not dispatched to their expected discharge position. However, these assets are often then compensated when they are moved away from their charge profile, resulting in an incremental payment. This creates an opportunity for assets to be compensated, or made whole, when they are not run in line with their anticipated traded position. The impact on BM revenue on the overall monthly revenue is shown in Figure 3 below.

This highlights an important point for BESS participation in the SEM: revenue opportunity is highly variable. The data points to revenue distribution being sensitive to system conditions, renewable output, demand patterns, system limitations and the ability of optimisers to react quickly to market signals.

Follow PN: Improving Confidence in Dispatch

One of the most important elements of S&D for BESS assets was the introduction of Follow PN (or “Follow Physical Notification”). Under this arrangement, assets are expected to be dispatched close to or at their traded market position, outside of system security reasons. This provides certainty for asset owners to develop trading strategies around clear operational expectations.

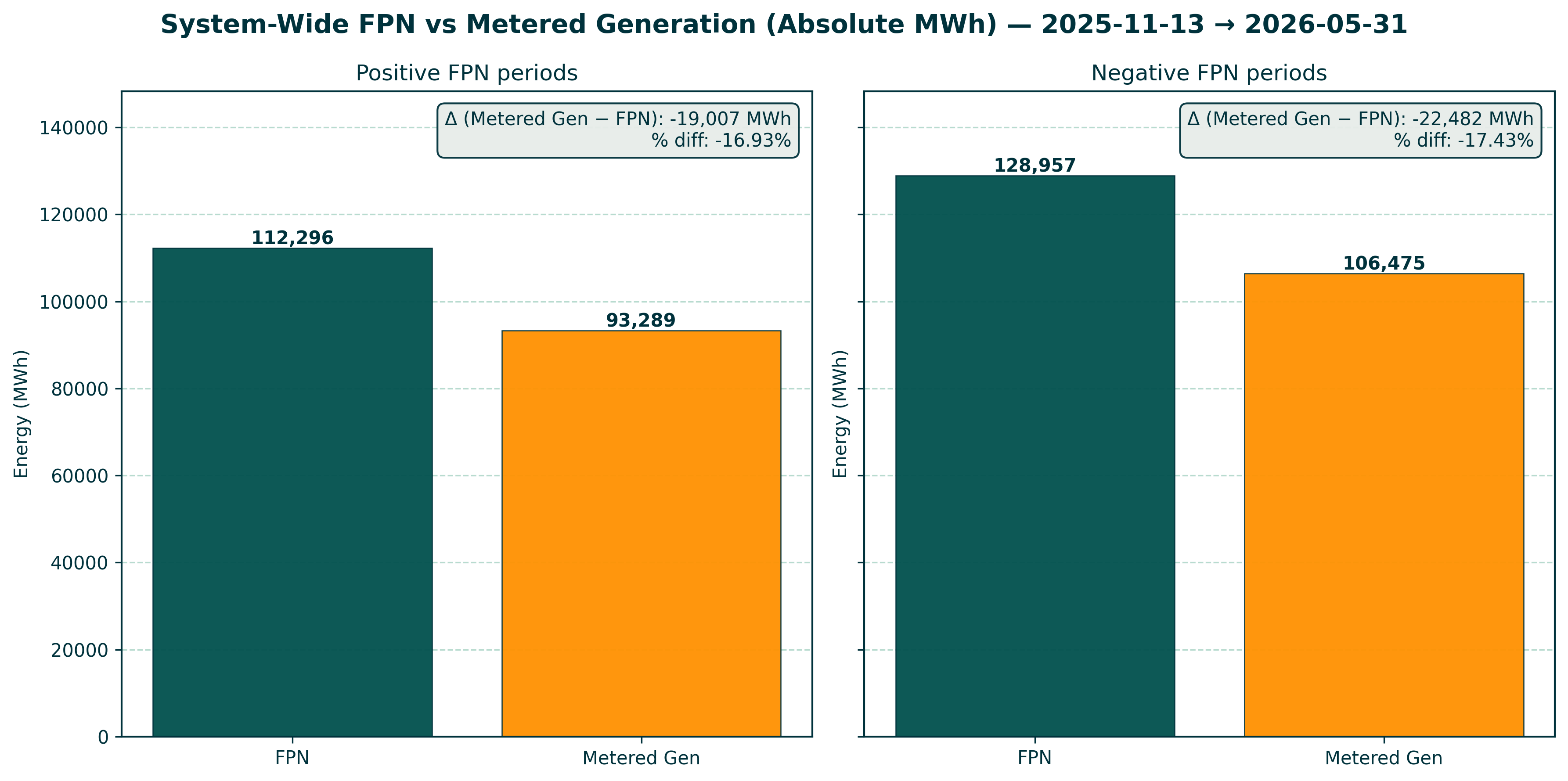

Our previous analysis identified that a significant proportion of traded positions, in excess of 20%, were not being followed by the TSO. Figure 4 shows the slight improvement we have seen, with that figure now coming in at roughly 17% of volume deviating significantly from their traded positions. We hope to see continued improvements in this over the coming months.

While dispatch will never perfectly match trading positions due to real-time system requirements, the improvement is a positive signal for the industry. It demonstrates continued progress as operational processes mature.

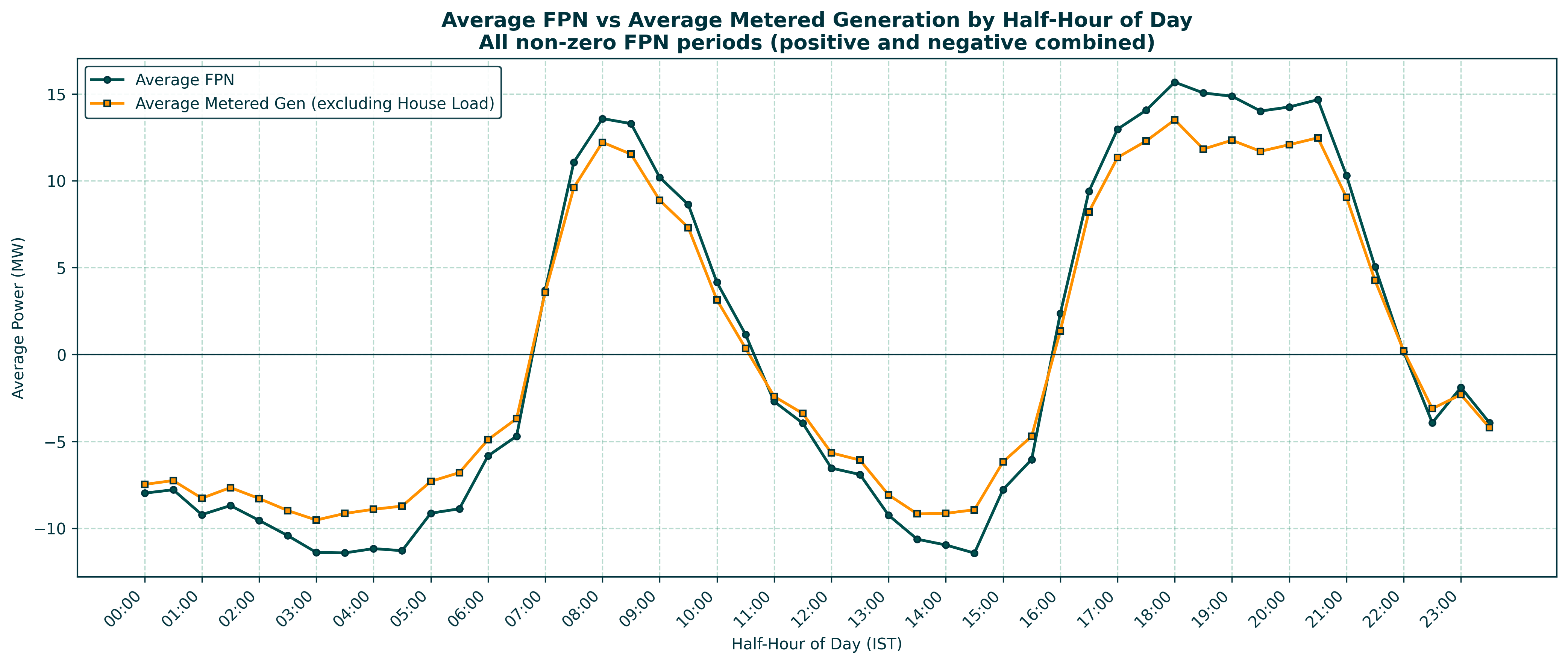

As can be seen in Figure 5, the largest differences remain around periods of system stress, particularly during evening peaks when renewable availability, SNSP levels and system constraints become key considerations for the TSOs. In this scenario, the TSOs seem less willing to dispatch BESS assets at the cost of curtailing renewables. This lines up with what was articulated in the communications with the industry by the TSO prior to the delivery of the S&D program.

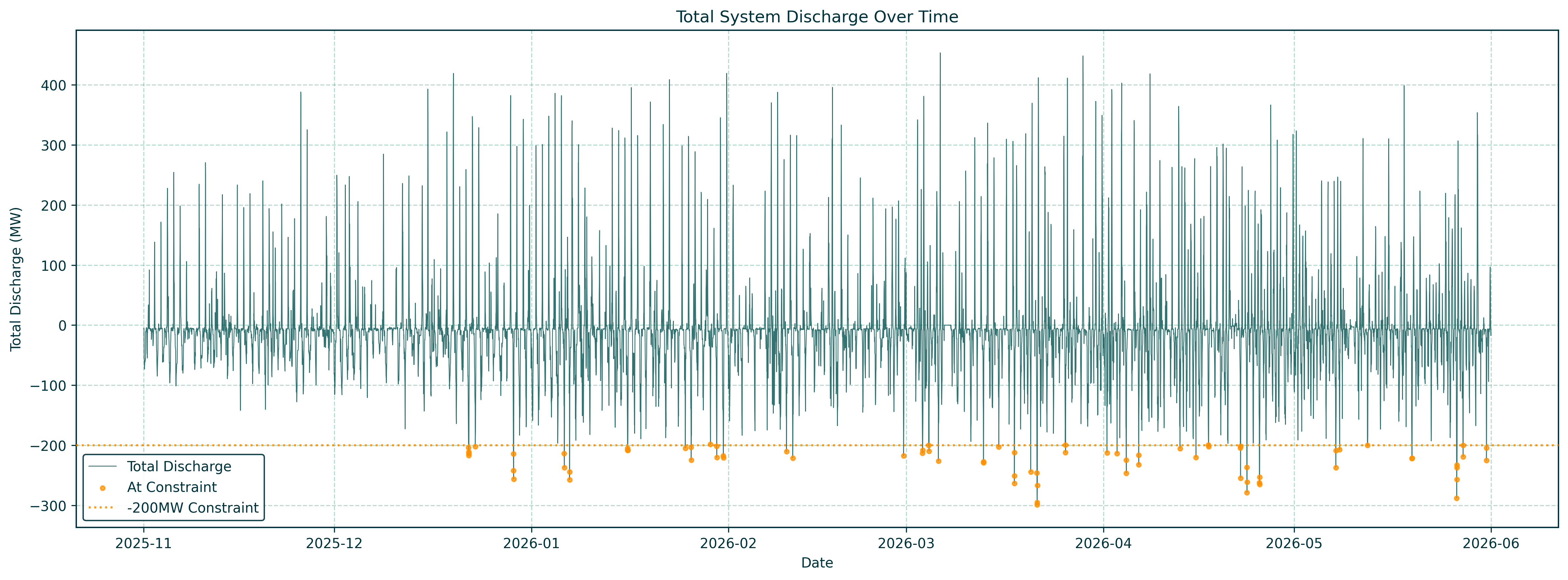

Following the implementation of S&D, BESS charging was initially subject to a blanket constraint limiting assets to 20% of their Maximum Import Capacity (MIC). This was quickly replaced by a group-wide constraint that limits charging when the combined BESS charging profile exceeds 200MW.

However, our graph in Figure 6, of the dispatch data suggests this is not operating as a fixed cap. Instead, TSO appear to be managing the constraint dynamically, allowing greater charging volumes when system conditions allow. This approach provides flexibility for assets while balancing the operational requirements of the system.

While a significant portion of the BESS fleet remains non-firm and is therefore not compensated when dispatched below its expected discharge position, these events can create secondary market opportunities. If an asset is not discharged as expected, its State of Charge (SoC) remains higher than forecast, which can prevent it from reaching its traded charging position for the following morning. In these circumstances, assets may submit incremental offers into the Balancing Market (BM), creating an additional route to capture value.

The Evolution of BESS Trading Strategies

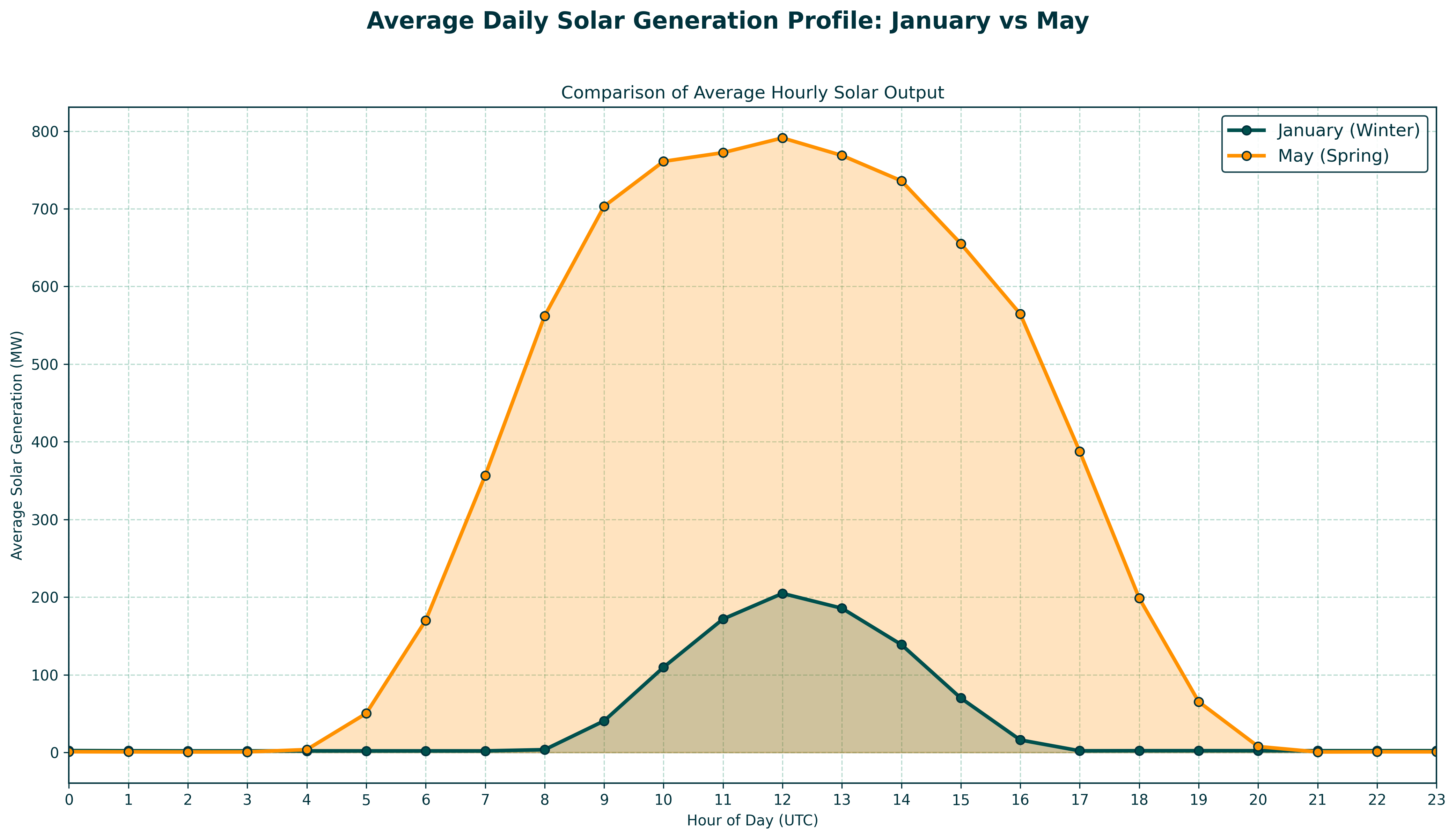

The market opportunity for batteries has continued to evolve since the introduction of S&D. During the early stages, trading strategies were heavily focused around capturing the evening peak. We can see in Figure 9 that this has changed over the past few months, with more volume focused on the morning peak, and charging through the midday price reduction. However, the usual movement in prices over the change in seasons, helped by a growth of solar generation (as can be seen in Figure 7) has changed the daily price profile, creating the possibility of a second daily trading opportunity, with batteries increasingly able to optimise around both morning and evening peaks.

While the price curve reflects the change in daily demand profile over the summer months, the significant increase in solar output creates a more pronounced price curve (often referred to as the duck curve). Notably, this has been developing year on year as both the wholesale and behind the meter solar capacity has rapidly grown.

The result of this is lower midday prices, which have created an additional opportunity for batteries to charge during periods of high renewable output and discharge later when demand increases.

With the continued success of RESS in supporting solar projects and the expected maintenance of rooftop solar grants through the term of the current government, this trend is likely to continue. Batteries that can adapt their strategies around changing market conditions will be best positioned to capture these opportunities.

Future of the Industry

The introduction of Schedule & Dispatch has fundamentally changed the role of, and opportunity for, BESS assets in the SEM.

While the programme is still developing and operational challenges remain, asset owners and optimisers now have greater access to energy markets and a clearer framework to develop trading strategies.

Additional clarity across several key workstreams is needed to unlock the full potential of the Irish storage market. In particular, the industry would benefit from firm timelines and early design details for the enduring BESS reforms being delivered through the Strategic Market Programme. These changes should enable greater market-based BM redispatch and, if implemented effectively, could further differentiate Ireland from other European markets, where BM revenues already form a significant component of the BESS revenue stack.

DASSA is also beginning to take shape. While the complexity of the market design will require a period of adjustment, it is likely to create opportunities for innovative trading strategies. The publication of the first Annual Reserve Service Forecast later this year will be a key milestone, providing the industry with greater visibility of the revenue potential available through this new market.

The planned change in network charges (announced this month by the CRU) from October 2026 is a welcome change. BESS units will now be charges as generators rather than demand customers. Not only does this align procedures across the SEM, we are confident that this will increase the use of BESS units, providing more flexibility to the grid, as well as more revenue opportunities for owners.

ElectroRoute continue to actively analyse the commercial prospect of floors, tolls and swaps and while the market is not as advanced as that of our neighbours in Great Britain or indeed Germany, the direction of travel of policy suggests that there will be opportunities to enter into floor arrangements.

However, for a meaningfully competitive and deep contracting market to emerge beyond a small number of flagship announcements, it is essential meaningfully progress is made on policy initiatives around S&D, strategic market reform, DASSA, LDES (EirGrid and ESBN) and hybrid design over the course of the next 6-12 months.

For a trading/optimising entity to agree to take on 7-12 years of risk through a floor/toll, it is essential that there is reasonable clarity and confidence on the direction of travel for these initiatives, particularly given the likely impact of each on system and pricing dynamics.

If you would like to discuss opportunities in the Irish storage market, we will be attending the ESI conference on the 30th of June in Croke Park and would be happy to meet in person. Please feel free to get in touch with our Storage Lead at rory.cafferky@electroroute.com.