EU Gas Market Interventions: The Good, The Bad and The Downright Ugly

EU Gas Market Interventions: The Good, The Bad and The Downright Ugly

Introduction

With the recent energy price volatility experienced across Europe, the European Union has taken dramatic steps to protect its markets and citizens from these effects and to safeguard future supply. In this article, we will explore the proposed solutions laid out by the EU to reduce the volatility of gas contracts at the TTF Hub, as well as their expected benefit for European consumers and the potential drawbacks for the wider gas market.

Background

Energy prices across Europe fluctuated wildly because of the Russian invasion of Ukraine which saw Russian gas flows first reduce from 39.7% in 2021 of EU imports to 22.9% in Q2 2022 and then cut off, a tight global market for LNG and a large and extended series of French Nuclear power outages.

The European Union agreed on a set of temporary Gas Market interventions, to help rein in extreme energy price volatility experienced over the prior 24 months across Gas Contracts at the TTF Hub. These measures focused on three key areas:

- Joint Gas Buying.

- A New LNG Price Index.

- An Intraday Trading Circuit Breaker.

These gas market correction mechanisms will apply for one year from February 15th and apply for a period of 1 year.

Interventions

1. The joint buying plan aims to stop EU companies from outbidding each other for at least a portion of their required gas supplies and to focus attention on filling gas storage facilities for winter 2023/2024. The plan would require companies to pool gas demand equal to 15% of their storage obligations next winter and seek suppliers through the new EU energy platform.

2. The new LNG price index plan aims to give buyers a stable and predictable alternative to the TTF price benchmark for pricing LNG contracts. EU energy agency ACER had to start publishing a daily LNG price assessment based on actual trading data for all LNG imports to Europe within two weeks of the new interventions becoming binding. The first published LNG gas price assessment for NWE was 56.77€/MWH. The publication was delayed due to insufficient uptake from market participants.

3. The Intraday Trading Circuit Breaker would see the TTF market be capped based on the average market price for a set number of days, rather than the current spot price, which may have spiked.

Triggers

The Market Intervention Mechanisms will be automatically triggered if two key conditions are met:

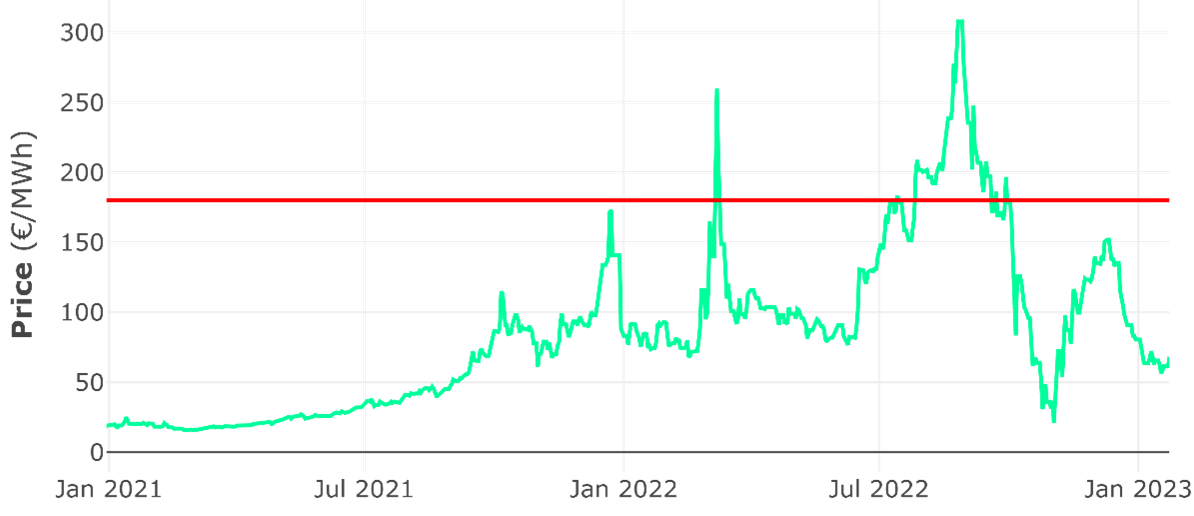

- (Price) 1-month FWD TTF Settlement price is > 180€/MWh for 3 days.

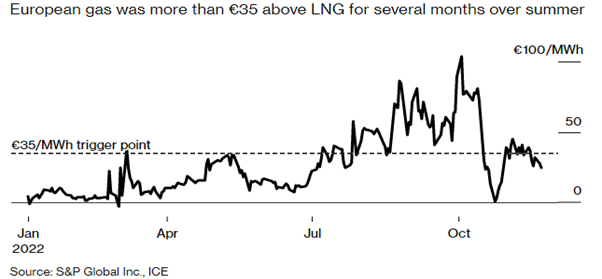

- (Spread) TTF Price is 35€ > LNG reference price during the last 3 days.

Once triggered, it will remain in place for at least 20 working days. It will also apply to all EU gas-trading hubs, with a possibility to opt out later.

Analysis of Measures

The hope is that suppliers and consumers would voluntarily start using this as a reference price in their contracts and that once established it could be used to hedge LNG prices and other gas prices through derivative contracts. However, the plans have split member states, along a North-South axis, with southern and eastern countries largely in favour of measures to curb unprecedentedly high prices.

If the cap had been introduced at the start of this year, it would have been used on more than 40 days in August and September

While intended to help Europe cope with the energy crisis it may have the inverse effect and lead to a series of unintended consequences with knock-on effects.

1. Inefficient Price Signals

Without any countermeasures to actively react to any unintended consequences of a TTF price, it is likely that the market will not provide efficient price signals that would encourage users to reduce their gas demand and incentivise producers to increase supply.

2. A shift to OTC.

The proposed cap only applies to TTF contracts with specific maturities, including the Front month contract. The cap doesn’t extend to OTC trading, carried out by brokers. This would mean that at higher prices trades could still happen in all other TTF markets, and all contracts traded OTC and in the spot market.

3. Reduced Liquidity

An inevitable consequence of implementing market interventions is that they create unintended consequences for the behaviour of market prices as they near a cap. It is hard to quantify the effect as each market participant will hold individual expectations of trading strategies and expectations of other market participants’ reactions.

4. Long-Term Gas Market Effects.

The overarching view of the EU along with many western nations is the phase-out of fossil fuel reliance and technology. Any intervention that leads to or potentially signals lower liquidity and less efficient price signals could have spillover effects for investment signals for renewables and low-carbon investments.

Conclusion

The risk of unintended consequences and the proposals will do nothing to ease Europe’s supply crises. Instead, the rushed-through laws could exacerbate the current liquidity crises in wholesale markets, create financial instability and drive companies away from Europe. With a limit to what contracts are capped, there is the potential that if the cap was to be triggered, we would not actually see a cap in wholesale gas prices as contracts with similar characteristics could be traded OTC.

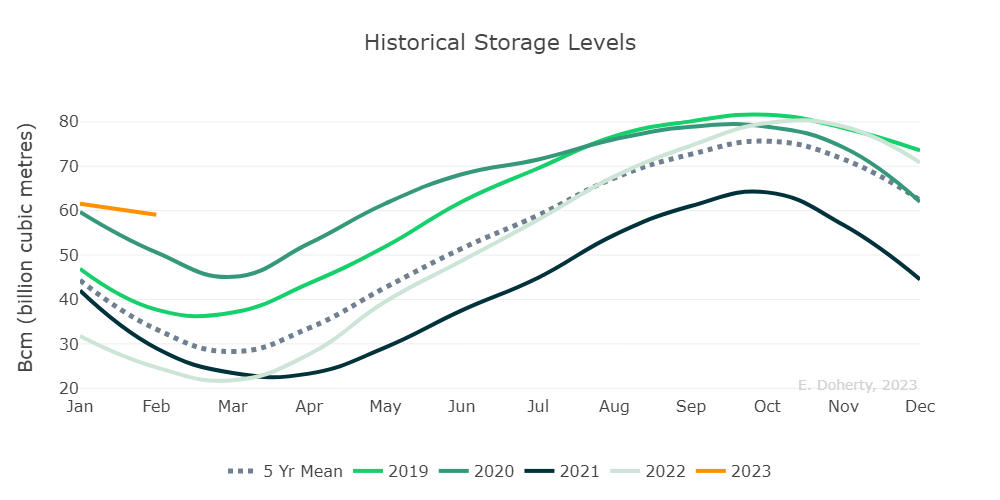

With current price levels on the retreat from 338€/Mwh in August 2022 to 53€/MWh in Mid-February 2023, gas levels in storage across Europe currently stand at over 50% full compared to 26% for the same period last year. We may not see the measures activated, but the knowledge that the market has fundamentally changed the rules of engagement will leave a subconscious bias on those who choose to participate.

ICE, which hosts the benchmark Dutch contract, said it is reviewing the details of the EU plan to assess whether it can continue to operate fair and orderly markets for TTF from the Netherlands as per our European regulatory obligations. The exchange previously voiced concerns about the destabilizing impact a cap would have on the market, but it said trading will continue to operate as usual.

Article written by John O’Brien.

If you would like to speak to ElectroRoute about our services, please email us at info@electroroute.com